20

20

Technology

Shares of NIO, a China-based electric car manufacturer, are soaring this morning after the companyQ3 2019 earnings beat investor expectations. NIOsurprise win comes directly on the heels of Tesla, a competitor, announcing the delivery of its first cars made in China, NIOhome market.

NIO went public on the New York Stock Exchange in 2018 for $6.26 per share. Its value has plunged as a public company, seeing its per-share price fall to as little as $1.19. Today, after its earnings report, NIO shares are up more than $1 apiece, to $3.47 per share as of the time of writing. That new price represents a gain of a touch less than 44% in todaytrading.

Earnings

NIO managed to beat both revenue and profit expectations in the quarter. And, the companyforecast for its next quartercar deliveries show a sharp rise in automotive deliveries.

According to Yahoo Finance, investors expected NIO to lose $0.34 per share in Q3 on an adjusted basis off revenue of $230.8 million. In fact, NIO reported $257.0 million in revenue leading to an adjusted $0.33 per share loss. NIO managed a top-and-bottom beat while growing its total revenues by 21.8% compared to the sequentially preceding quarter, and 25% compared to the year-ago period.

While NIO did beat expectations, it remains a company deep in its investment cycle. Thata polite way of saying that it loses lots of money. For example, in its most recent quarter, NIOgross margin on selling automobiles came to -6.8%. That was a bit worse than its year-ago result of -4.3%, if better than what it managed earlier in Q2 2019.

NIOcore business can&t even cover its cost of revenues, let alone the operating costs of the rest of the company. This means that the company is consuming cash, putting an end date on its ability to operate without more cash.

As NIO put it in its earnings letter (emphasis: TechCrunch):

The Company operates with continuous loss and negative equity. The Companycash balance is not adequate to provide the required working capital and liquidity for continuous operation in the next 12 months. The Companycontinuous operation, which has also constituted the basis of preparing the Companythird quarter unaudited financial information, depends on the Companycapability to obtain sufficient external equity or debt financing. The Company is currently working on several financing projects, the consummation of which is subject to certain uncertainties. The Company will announce any material developments or information subject to the requirements by applicable laws.

So, NIO needs more money. Luckily for it, with a newly risen share price the firm has a better shot at selling more of itself to raise the capital it needs to stay in business and grow.

And grow it intends, with a written expectation of delivering &over 8,000& vehicles in Q4 2019, which it notes is about two-thirds more than it managed in Q3 2019; so NIO is telling investors that its revenue will be sharply higher in the current period than it was in the preceding three-month period.

All good news for NIO, even if Musk and company are breathing down its neck. And good news for the 2018 IPO class.

- Details

- Category: Technology

Read more: China-based NIO’s shares skyrocket as the Tesla rival beats investor expectations

Write comment (95 Comments)

We love parties almost as much as we love startups, but we go absolutely bonkers for a hot startup/party mashup. Thatwhy we&re returning to host our 3rd Annual TechCrunch Winter Party in San Francisco on Friday, February 7. Even better news, party-goers — additional (the second batch) coveted tickets to this wild winter romp are available now. Better get your tickets while you can.

Last yearinaugural event was a huge success, as nearly 1,000 of Silicon Valleybrightest minds came to relax, connect and celebrate the entrepreneurial spirit of the startup community — and cast a keen eye over some promising startups.

This yearsoiree takes place at Galvanize and features tasty libations, delicious hors d&oeuvres and engaging conversation. That sounds so very civilized, right? Well, don&t dry clean your stuffed shirt just yet, because we&ll have plenty of party games and activities, giveaways and fun surprises. And, of course, plenty of photo ops, baby!

Galvanize may be a multi-level venue, but the space is still limited — as are the tickets. We&re rolling them out in batches over the next few weeks, so keep checking back if you can&t snag a ticket.

Here are the pertinent Winter Party details:

When: Friday, February 7, 6:00 p.m. & 9:00 p.m.Where: Galvanize, 44 Tehama St., San Francisco, CA 94105Ticket price: $85 (buy them here)

Hereanother great idea. Why just mingle and schmooze when you can mingle, schmooze and demo your early-stage startup in front of hundreds of the Valleytop star-makers? Buy a demo table for $1,500 (the price also includes four attendee tickets). Demo tables are limited, so act now before other founders snatch &em up.

Of course, no TechCrunch party is complete without plenty of awesome prizes, including TC swag and tickets to Disrupt San Francisco 2020. Come on out for a great midwinternight of relaxed connection, fun and opportunity. Get your tickets to the 3rd Annual TechCrunch Winter Party at Galvanize today.

- Details

- Category: Technology

Read more: Buy your tickets to the 3rd Annual TechCrunch Winter Party

Write comment (91 Comments)Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Itthe second to last day of 2019, meaning we&re very nearly out of time this year; our space for repretrospection is quickly coming to a close. Before we do run out of hours, however, I wanted to peek at some data that former Kleiner Perkins investor and Packagd founder Eric Feng recently compiled.

Feng dug into the changing ratio between enterprise-focused Seed deals and consumer-oriented Seed investments over the past decade or so, including 2019. The consumer-enterprise split, a loose divide that cleaves the startup world into two somewhat-neat buckets, has flipped. Fengdata details a change in the majority, with startups selling to other companies raising more Seed deals than upstarts trying to build a customer base amongst folks like ourselves in 2019.

The change matters. As we continue to explore new unicorn creation (quick) and the pace of unicorn exits (comparatively slow), italso worth keeping an eye on the other end of the startup lifecycle. After all, what happens with Seed deals today will turn into changes to the unicorn market in years to come.

Letpeek at a key chart from Feng, talk about Seed deal volume more generally, and close by positing a few reasons (only one of which is SnapIPO) as to why the market has changed as much as it has for the earliest stage of startup investing.

Changes

Fengpiece, which you can read here, tracks the investment patterns of startup accelerator Y Combinator against its market. We care more about total deal volume, but I can&t recommend the dataset enough if you have the time.

Concerning the universe of Seed deals, hereFengkey chart:

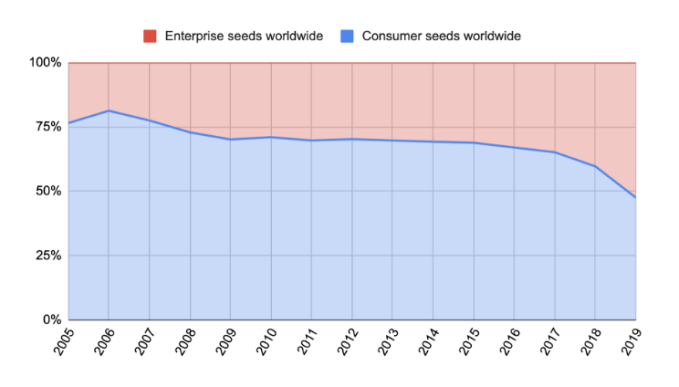

Chart via Eric Feng / Medium

As you can see, the chart shows that in the pre-2008 era, Seed deals were amply skewed towards consumer-focused Seed investments. A new normal was found after the 2008 crisis, with just a smidge under 75% of Seed deals focused on selling to the masses for nearly a decade.

In 2016, however, a new trend emerged: a gradual decline in consumer Seed deals and a shift towards enterprise investments.

This became more pronounced in 2017, sharper in 2018, and by 2019 fewer than half of Seed deals focused on consumers. Now, more than half are targeting other companies as their future customer base. (Y Combinator, as Feng notes, got there first, making a majority of investments into enterprise startups since 2010, with just a few outlying classes.)

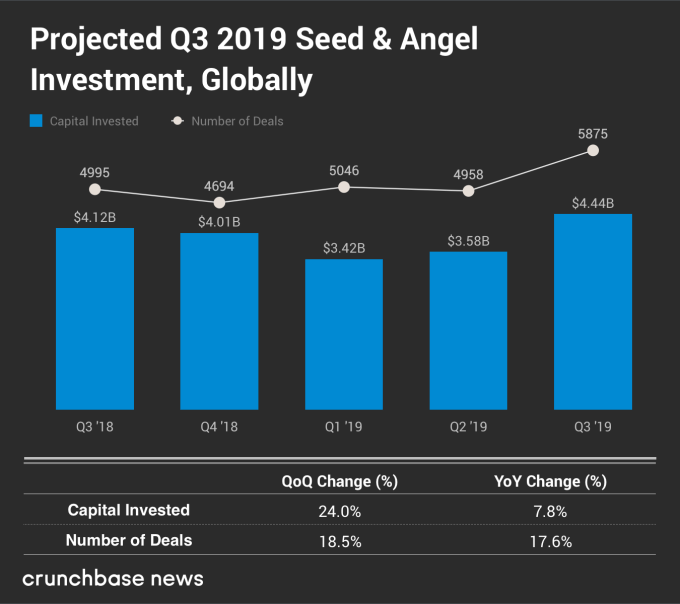

This flip comes as Seed deals sit at the 5,000-per-quarter mark. As Crunchbase News published as Q3 2019 ended, global Seed volume is strong:

So, we&re seeing a healthy number of deals as the consumer-enterprise ratio changes. This means that the change to more enterprise deals as a portion of all Seed investments isn&t predicated on their number holding steady while Seed deals dried up. Instead, enterprise deals are taking a rising share while volume appears healthy.

Now we get to the fun stuff; why is this happening?

Blame SaaS

As with many trends long in the making, there is no single reason why Seed investors have changed up their investing patterns. Instead, there are likely a myriad that added up to the eventual change. I&m going to ping a number of Seed investors this week to get some more input for us to chew on, but there are some obvious candidates that we can discuss today.

In no particular order, here are a few:

- SnapIPO: Snap went public in early 2017 at $17 per share. Its equity quickly spiked to into the high 20s. By July of that same year, Snap slipped under its IPO price. Its high-growth, high-spend model was under attack by both high costs and slim gross margins. Snap then went into a multi-year purgatory before returning to form — somewhat — in 2019. Itnot great for a categoryinvestment pace if one of its most prominent companies stumble very publicly, especially for Seed investors who make the riskiest bets in venture.

- Details

- Category: Technology

Read more: Seed investors favor enterprise over consumer for first time this decade

Write comment (99 Comments)Itthe slowest week of the year for gadget news. Christmas is in the rearview, and ita few days until the new year. After that, ita straight shot to CES and then MWC. Meantime, best we&ve got going for us are a handful of rumors, including a peek at what Googlenext budget handset might could potentially possibly conceivably look like.

Per renders from OnLeaks and 91Mobiles, a vision of the Pixel 4a has appeared — or, a render, rather. The handset will no doubt be an important one for Google. After all, the 3a (pictured at top) helped the company recover from some lackluster sales last year. A couple of pieces jump out at first glance. The display appears to finally buck the companylongtime notch dependency, in favor of a hole punch camera on the front.

![]()

Perhaps even more compelling, the device seems to hold the torch for the headphone jack. In 2020, that could well be a standout feature even among mid-range handsets. As the company eloquently put it around the time of the 3arelease, &a lot of people have headphones.&

Other notable features on the forthcoming device includes the addition of the squircle phone bump on the rear, a design element borrowed from the Pixel 4. Likely the handset will stick to a single camera, instead of adopting the flagshiptruly excellent dual-camera setup. Even so, Googlebeen able to accomplish some solid imaging technology with just the one sensor, courtesy of clever ML software.

The display, too, will be slightly larger than its predecessor, bumping up one or two tenths of an inch. The handset is reportedly dropping around May, probably just in time for I/O 2020.

- Details

- Category: Technology

Read more: Google Pixel 4a renders include a headphone jack and hole-punch display

Write comment (95 Comments)

VMware is closing the year with a significant new component in its arsenal. Today it announced it has closed the $2.7 billion Pivotal acquisition it originally announced in August.

The acquisition gives VMware another component in its march to transform from a pure virtual machine company into a cloud native vendor that can manage infrastructure wherever it lives. It fits alongside other recent deals like buying Heptio and Bitnami, two other deals that closed this year.

They hope this all fits neatly into VMware Tanzu, which is designed to bring Kubernetes containers and VMware virtual machines together in a single management platform.

&VMware Tanzu is built upon our recognized infrastructure products and further expanded with the technologies that Pivotal, Heptio, Bitnami and many other VMware teams bring to this new portfolio of products and services,& Ray O&Farrell, executive vice president and general manager of the Modern Application Platforms Business Unit at VMware, wrote in a blog post announcing the deal had closed.

Craig McLuckie, who came over in the Heptio deal and is now VP of R-D at VMware, told TechCrunch in November at KubeCon that while the deal hadn&t closed at that point, he saw a future where Pivotal could help at a professional services level, as well.

&In the future when Pivotal is a part of this story, they won&t be just delivering technology, but also deep expertise to support application transformation initiatives,& he said.

Up until the closing, the company had been publicly traded on the New York Stock Exchange, but as of today, Pivotal becomes a wholly owned subsidiary of VMware. Itimportant to note that this transaction didn&t happen in a vacuum, where two random companies came together.

In fact, VMware and Pivotal were part of the consortium of companies that Dell purchased when it acquired EMC in 2015 for $67 billion. While both were part of EMC and then Dell, each one operated separately and independently. At the time of the sale to Dell, Pivotal was considered a key piece, one that could stand strongly on its own.

Pivotal and VMware had another strong connection. Pivotal was originally created by a combination of EMC, VMware and GE (which owned a 10% stake for a time) to give these large organizations a separate company to undertake transformation initiatives.

It raised a hefty $1.7 billion before going public in 2018. A big chunk of that came in one heady day in 2016 when it announced $650 million in funding led by Ford$180 million investment.

The future looked bright at that point, but life as a public company was rough, and after a catastrophic June earnings report, things began to fall apart. The stock dropped 42% in one day. As I wrote in an analysis of the deal:

The stock price plunged from a high of $21.44 on May 30th to a low of $8.30 on August 14th. The companymarket cap plunged in that same time period falling from $5.828 billion on May 30th to $2.257 billion on August 14th. Thatwhen VMware admitted it was thinking about buying the struggling company.

VMware came to the rescue and offered $15.00 a share, a substantial premium above that August low point. As of today, itpart of VMware.

- Details

- Category: Technology

Read more: VMware completes $2.7 billion Pivotal acquisition

Write comment (100 Comments)

Satellite industry giant Maxar is selling MDA, its subsidiary focused on space robotics, for $1 billion CAD (around $765.23 million USD), Reuter reports. The purchasing entity is a consortium of companies led by private investment firm Northern Private Capital, which will acquire the entirety of MDACanadian operations, which is responsible for the development of the Canadarm and Canadarm2 robotic manipulators used on the Space Shuttle and the International Space Station, respectively.

Maxargoal in selling the business is to help alleviate some of its considerable debt, which stood at $3.1 billion as of this past September. The company was already known to be seeking potential buyers for MDA, so itnot much of a surprise. MDA will continue to operate as its own company under the terms of the new ownership, which should mean that its current plans and contracts will continue.

MDA is working on a number of projects for various clients, including developing wildfire-monitoring satellites, navigation antennas for use on other companysatellites and to develop Canadarm3, the next version of its robotic appendage, for use on the NASA Lunar Gateway that will be a research and staging station orbiting the Moon as part of the U.S. space agencyArtemis mission series.

- Details

- Category: Technology

Read more: Maxar is selling space robotics company MDA for around $765 million

Write comment (97 Comments)Page 21 of 5614